My Reaction

J. Carlton Collins reaction to Best Software’s Response

June 1, 2005

I first published the report “How Great Plain beats MAS

90” in March 2005 in conjunction with a paid one-hour presentation at

Microsoft's Partner Conference where I was asked to help Great Plains

resellers sell against MAS 90.

Surprisingly, Best Software officials are upset with

me for publishing this report. If they took a step back for a moment they

would realize that I positioned Great Plains and MAS 90 as the two top

accounting system products in the world - that's a pretty good endorsement

coming from a nationally recognized, impartial accounting systems

consultant. In addition, in at least six different areas in my report I

delivered high praise for MAS 90.

Best's problem is that my report

points out dozens of areas where Great Plains provides features and

functions better than does MAS 90 - and they are sore at me for exposing

their shortcomings. For the record, I am a fan of MAS 90. I do believe it is

a top product. But if you stack the top two sprinters in the world side by

side in the Olympics, only one is going to come out on top. That is no

disrespect to the silver medal winning sprinter - that's just the way it is.

In a rather pissiant move, Best's officials issued a response to my report which you

can read by

clicking here. In their response, Best officials make four

points in an attempt to discredit my original report. I have addressed each of their points below.

This response was issued the day after Best released their Response.

- "Collins was not independent with

respect to the report"

This point is absolutely true as I was not independent with respect to the preparation of this report. I stated this fact several times in the report. This report was delivered at the Microsoft Partner’s conference and my intent was to help these MBS resellers sell against MAS 90. The report was a by-product of this presentation. While this report was indeed one-sided (a fact which was disclosed), I would argue that my body of work shows that I strive to be independent. For example, 22 months ago I published reports showing how Best’s ACCPAC product beats Great Plains and another report showing How Best’s ACCPAC product beats Navision. In 2003, I also developed and delivered an 8 hour seminar featuring all of the Best products and demonstrated them live across the country. This course was highly rated and featured a live demonstration of MAS 90, MAS 500, ACCPAC Advantage, ACCPAC ProSeries, Abra, FAS, ACT!, Sales Logix, MIP, CPA Software, BusinessVision 32, Peachtree, and other Best products. The course took me approximately 5 months to develop, and I signed up 167 BSAN partners as part of this seminar series. The following year I did the exact same thing focusing on Microsoft products. I have recently published reviews of non Microsoft and non Best products as well. I ask you - do my efforts sound biased?

- "Factual Inaccuracies"

Best claims that my paper had factual errors, and they cite seven specific examples. Each of these seven examples is discussed below:

- The first example Best cites refers to page 15 under the sub title “Number of Open Periods” My point was that MAS 90 provides only 26 months open periods in the GL. However I did not repeat the word "open" in the second sentence. When read in context with the previous sentence I think the point is obvious. The subtitle of this paragraph also makes the point obvious. However, Best has zeroed in on the second sentence, taken it out of context, and suggested that I made an error by suggesting that I said MAS 90 supports only 24 periods, when I clearly meant that MAS 90 supports only 24 open periods. To avoid any further confusion, I have edited my document by adding the word “open” to this second sentence.

- The second example Best cites discusses landed costs after the invoice has been processed as discussed on Page 25 – Best officials state that they provide landed costs abilities, and I agree that they do. However the point that I make was that this feature is not supported in MAS 90 after the invoice has been received, processed, and posted. The information I used as a basis for this comment was supplied by the MAS 90 product manager to Software Solutions in 2005 and was certified by Charles Chewning in the latest edition of the Accounting Library as shown in the partial report below (highlighted in yellow).

Therefore if this is indeed an error on my part, it started with information originally provided by Best Software officials. I still think that my comment was accurate, and that Best took liberties here by stretching my comment to imply more than it did.

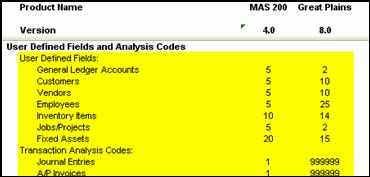

- The third example Best cites involves user definable fields as discussed on page 12 – To make the claim that I am in error, Best officials had to reach into their bag of undocumented features. Officially, Best has always reported that that a certain number of user definable fields are available in MAS 90/200, but evidently the total fields are limited to the number of characters used to describe each field. Therefore if you use brief field descriptions, you can create more user definable fields. I searched through the MAS 90 help files, several dozen MAS 90 reseller sites, and the Best Software web site - and nowhere can I find a mention of this expanded description of user defined fields. The MAS 90 resellers I checked with were also unaware of this expanded description. Therefore I guess you need to be a MAS 90 programmer to know about this hidden tidbit. The information I used as a basis for this comment was supplied by MAS 90 product managers and was certified by Charles Chewning in the latest edition of the Accounting Library as shown in the partial report below (highlighted in yellow).

Therefore if this is indeed an error on my part, it started with information originally provided by Best Software as shown above.

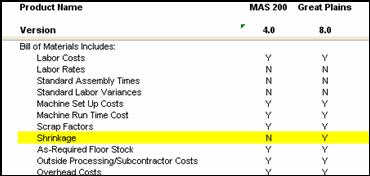

- The fourth example Best cites involves scrap discussed on page 29 – Apparently Best officials believe that the “shrinkage” function (which they admit is not included in MAS 90) can be solved using their “scrap” functions. After thinking about this a little while and working it in the MAS 90 system, I think that they are correct. I did explain in my disclosure statement that there may be clever work-around procedures that MAS 90 users can employ to overcome some of the weaknesses exposed in this report. This seems to be a decent work-around for the missing shrinkage function. Once again, the information I used as a basis for this comment was supplied by the MAS 90 product manager and was certified by Charles Chewning in the latest edition of the Accounting Library as shown in the partial report below (highlighted in yellow).

I would recommend that Best officials provide this updated information to the Software Solutions as the current edition of the Accounting Library reflects that shrinkage is not available in MAS 90.

- The fifth example Best cites involves Visual Basic functionality discussed on page 17 – Best officials point out that Visual Basic scripting is available in the Customizer module. I have confirmed that this is true. I have long shown audiences and end users how to customize MAS 90/200 using the built-in tools, but I have never shown this particular Visual Basic scripting capability. I wish that I could report to you that I was unaware of this feature in MAS 90/200, but I see that I actually published a review of MAS 90 several years ago where I mentioned this Visual Basic capability. This was my mistake and I concede this point. The mistake was not intended. I am only interested in publishing accurate information. I have edited the appropriate sentence on page 17 to reflect this fact accurately.

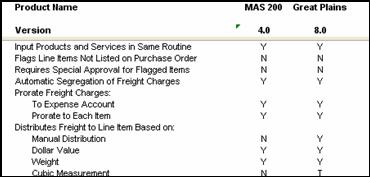

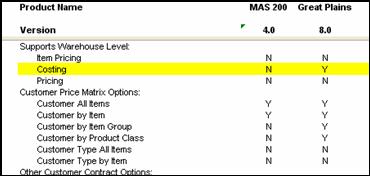

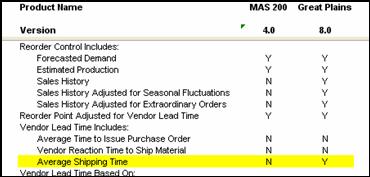

- The sixth example Best cites involves costing by warehouse location and vendor lead times as discussed on page 28 – To make this claim Best asserts that they offer these two features but Best officials do not give any details - instead they claim that MAS 90/200 handles both of these features. However, the information I used as a basis for this comment was supplied by the MAS 90 product managers and was certified by Charles Chewning in the latest edition of the Accounting Library as shown in the two partial reports below (highlighted in yellow).

If MAS 90/200 does indeed support these two features, then why did Best Officials report otherwise to Software Solutions? The information shown in the report above was provided to Software Solutions by Best officials in 2005 and I relied on this information in the preparation of the report. Since Mr. Chewning requires the vendor to demonstrate each feature they claim to have individually, I tend to believe that’s Mr. Chewning’s information is correct. If indeed MAS 90/200 does provide these capabilities, then why did they not demonstrate them to Mr. Chewning? In a quick search of the MAS 90 user screens, I could not find these features. I do not deny that these features are there, but I must insist that Best show them to us. In the absence of any description of this capability, and in the absence of being able to verify the existence of these features in the product myself, I will continue to rely on the information as reported to Software Solutions.

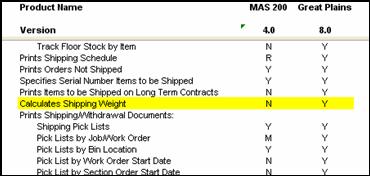

- The seventh example Best cites involves the calculation of shipping weight as discussed on page 30 – Best contradicts itself by claiming that the MAS 90/200 product performs this calculation and then claims that such calculations are not practical because packing material is not included. Well, which is it? If indeed Best believes that this feature is not useful, then I disagree. I believe that this feature is useful and widely used today. I also believe that companies can use a "imputed weight amount" that accurately reflects the weight of an item as well as any shipping material. I disagree that weighing all items after they have been boxed and then entering that information into the system to capture that data and to recreate new packaging slips is the most efficient procedure. The information I used as a basis for this comment was supplied by the MAS 90 product manager and was certified by Charles Chewning in the latest edition of the Accounting Library as shown in the two partial reports below (highlighted in yellow).

If MAS 90/200 does indeed support these two features, then why did Best Officials report otherwise? Therefore if this is indeed an error on my part, it started with information originally provided by Best Software as shown above.

- "Market Requirements"

Best Officials point out that their full range of products are designed to meet the needs of companies of all sizes and industries, and somehow suggests that my comparison of MAS 90 to Great Plains is therefore "useless". Their argument misses the point. For example, Best officials point out that MAS 500 provides multi-currency and inter-company and is highly scalable. So what? The comparison I made had nothing to do with MAS 500 – it was between Great Plains and MAS 90/200. Does Best suggest that MAS 90/200 customers should also purchase MAS 500 to compensate for missing functionality in MAS 90/200? Why even bring MAS 500 into the discussion? Suppose you were deciding to purchase a Ford Taurus versus a Chrysler Sebring – both of which are passenger cars. Would the fact that Ford also makes the Ford Expedition SUV have any impact on whether the Taurus or Sebring was better suited for your needs? Best seems to infer that somehow it would.

Best also suggests that technology is a less important consideration when evaluating accounting systems. Best officials and resellers have made this very statement to me several times. They claim that customers do not purchase accounting systems based on technology. My reply to this is that perhaps companies should place more emphasis on technology. Consider that Wal-Mart has used superior supply chain technology to push competitors K-Mart, Federated Department Stores, Macy’s, Davidson’s, and others into bankruptcy. Perhaps these struggling companies would embrace technology more if they had the chance to do it all over again.

What’s wrong with 10 to 15 year old technology you might ask? Consider the automobile you drive today. Does it have anti-lock brakes? Does it have airbags? Does it have hand cranks for rolling up the windows? Chances are good that you would not be satisfied today with a 10 to 15 year old automobile, even if it were in brand new condition with no miles. Why? Because new technologies have emerged that make today’s automobiles safer and more convenient to operate. For that matter, I do not see Best officials walking around with older "bag phones" which weigh 8 pounds, just the opposite they all seem to have the latest technology when it comes to the cellular phones they carry and use. Are we to believe that embracing the newer technologies only applies to automobiles and cellular phones, but not to accounting systems? Best officials seem to suggest that somehow older technology in an accounting system doesn't matter much when a company selects a new accounting system.

- "Unsupported Statements"

Best concludes their rebuttal by citing a series of unsupported statements that they claim I make in my report. Each of these citations are addressed below:

- Timing of MAS 90 DOS to MAS 90 Windows. Best officials claims that it took just three years, starting in 1996 to convert MAS 90 DOS to MAS 90 Windows. However I still have the post card that was mailed to me (and thousands of other CPAs) years before 1996 that included an image of the proposed windows-based MAS 90 product. Am I to believe that this post card announcing this effort was mailed years before they actually began that effort?

- MSDE outperforms the MAS 90 ISAM database. Best officials say that I have not backed up my claim that MSDE outperforms the MAS 90 ISAM database. Interestingly they do not deny that my statement is true, they simply infer that I have no benchmark evidence of this. I concur that database performance depends upon a great many factors, and I am sure that it is possible to create a benchmark that shows MAS 90 faster under specific conditions. However, I would guess that for a random sampling of companies with revenue in the $5 million to $25 million range, the MSDE database would consistently out perform the MAS 90/200 database as a general rule. I base this purely on anecdotes and discussions I have had with MAS 90 and Great Plains customers and resellers - and I still believe this general conclusion to be accurate.

- Score Card – Best officials discount my score card table claiming that there is no objective or scientific tests to back up the numbers included in this table. I agree, and I stated such as part of the score card. I guess by Best official standards, we should completely eliminate the Olympics because judges come up with a score for each gymnast without supplying a scientific or objective test as to how they arrived at that score. As stated in the report, the existence of a feature, or the depth of a feature is subject to open interpretation – I guess you could say that the beauty is in the eye of the beholder.

- $200 million customers – I do not have a profile on all Great Plains and MAS 90 customers, therefore I cannot support my claim that Great Plains has more $200 million with actual numbers, but I do have a strong basis for this opinion. I have attended Best and Great Plains conferences for many years and I have had discussions with hundreds of MAS 90 and Great Plains resellers over those years. I have also talked with hundreds of MAS 90 and Great Plains users over the years. It has been my informal observation that Great Plains has more larger customers than does MAS 90/200. I did provide 8 examples in the report to back up this claim and I did disclose that this report was based on opinion, and not fact.

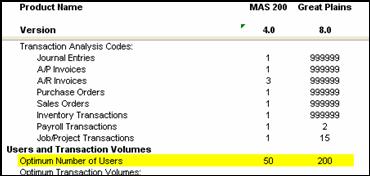

- Optimal Users – Best officials state that I have no basis for the optimal number of users I cite in the report. However, I do have a basis. Best's Presidient, David Butler, once told me in a conference metting (and other MAS 90 resellers on other occasions) that MAS 90 is officially positioned for up to 9 users. Further, the information Best officials reporting in the Accounting Library are shown in the partial TAL report below:

- XML – Best officials discount my praise for XML stating that XML is infrequently used. Three years ago, wireless networking was infrequently used. 10 years ago the Internet was infrequently used. 20 years ago, personal computers were infrequently used. According to the standard presented by Best, I guess we should not applaud any technology until it is "frequently used".

- Technologically Obsolete Posting and Closing Process – Best claims that I give no evidence that their closing process is technologically obsolete. Instead of addressing this issue, I will simply reprint this quote I received from an MAS 90 reseller a couple of weeks ago - One of the most annoying parts I find with MAS90 is how the transactions in a sub ledger get posted to the GL--having to specify a transaction update date when the data gets posted in the subledger. This not only affects/interferes with daily work-flow, it makes creating post-dated checks in AP a real nuisance. Obviously this MAS 90 reseller has a problem with MAS 90’s closing process.

Conclusion

As stated in the report, I firmly believe that both Great Plains and MAS 90/200 are both excellent products that are well supported by excellent companies and resellers. I stand by this statement.

In my opinion, the Best response makes two good points which I concede (shrinkage and Visual Basic) and I have edited my report to correct for these two points. As for the other points Best makes, I guess we will have to agree to disagree. After reading through the Best official’s response to this report, I stand firmly behind this report and I believe that the opinions and conclusions reached are reasonable and supported. Basically Best officials make a few nitpicking points, and most of those points can be traced back to inaccurate information provided by Best officials to harles Chewning and the Accounting Library. I find it hard to accept blame for any inaccuracies in this report that originated from Best officials in the first place.

I believe that disclosures make the reader aware that the report is opinionated and biased towards Great Plains. I have presented the entire report as opinion and advised readers to confirm any information before relying on that information. I am happy to publish the Best response next to the Great Plains / MAS 90 report in the interest of being fair and balanced and I will let the reader draw his or her own conclusions.

I invite you to submit your own comments to the discussion web on this topic.

Thank you.

J. Carlton Collins

Trademark Notices – Great Plains is trademark of Microsoft Corporation. MAS 90, MAS 200, and MAS 500 are trademarks of Best Software, a subsidiary of Sage PLC. QuickBooks is a trademark of Intuit, Inc.

Copyright June 2005, Accounting Software Advisor, LLC